Treading water keeps you afloat, but it doesn’t get you anywhere. You spend a lot of energy staying in one place. It’s exhausting.

‘Exhausted’ is exactly how I felt after my first year of trying to get on top of my finances.

I read and read through financial literature. My Podcast queue was filled with money advisors. I made and remade a budget almost every month. I researched all the latest budgeting tools and apps and set up meticulous spreadsheets, which I would adjust and reformat constantly, depending on the latest financial advice I read. I would hear about different investment strategies and go in circles trying to understand which one was best for me.

At the end of the year, I had made some financial gains, but I didn’t feel successful. I had invested enormous amounts of time, energy and mental stress for blah results. The truth is I was overwhelmed by the amount of information I found and confused by conflicting recommendations. I was stuck in analysis paralysis… I was treading financially.

My attitude and my situation changed, however, once I was able to narrow down my focus to one single number I could focus on to measure my financial success: my net worth. Once I started tracking that single number as my measure for success, I was quickly able to make significant progress in improving my financial situation.

Net Worth, Defined

I used to associate “net worth” with the rich and famous billionaires like Bill Gates or Warren Buffett. It know it sounds naive, but I didn’t even realize that I had a net worth (albeit on a MUCH more modest scale than those financial giants) until I started my own financial journey. Every single person has a net worth to manage, not just the world’s wealthiest.

So What is it exactly?

“Net worth is the amount by which assets exceed liabilities. A consistent increase in net worth indicates good financial health.”

Investopedia

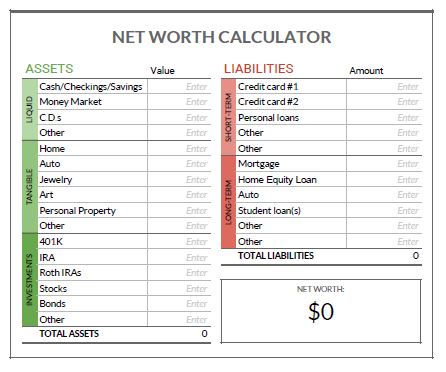

Essentially, you add up all the things you own of value, including checking accounts, savings accounts, 401Ks, IRAs, CDs, real estate, art, jewelry or anything else of value.

Then, you subtract from that total anything you owe, including credit cards, loans (car, student, personal), mortgages, HELOCs.

You can figure out your own net worth right now with this free Net Worth Calculator. It’s not important what your net worth is right now—it may even be a negative number. It doesn’t matter. What is important is to get a benchmark to measure your growth against.

Why this is important

If you look faaaar down the road and ever want to be able to retire, you are going to need to build up enough of a nest egg that you will be able to live the rest of your life without new money coming in. It will take you decades to build this, so don’t put this off mistakenly thinking you have time to do it later.

While retirement and living without an income may be the ultimate money goal, there are many other reasons to know and track your net worth that will serve as milestones along your financial journey.

Checking your net worth regularly is like a check-up for your financial health. It can tell you how you are doing and any areas you need to focus on at each stage of your life.

For example, if your net worth is a negative number, this indicates that you owe more than you own. There is nothing inherently wrong with this, but you ultimately want to be “in the black” so you now have a plan of action: Reduce your liabilities, or pay off your debt, until your net worth is a positive number – $1. That is a HUGE milestone to turn that corner, so make sure to celebrate when you reach this spot in your journey!

Or say you have a $1 net worth – that’s great you’re in the positive, but again, you will have indicators of what to do next when you look at the numbers. If you see that you have zero debt, but also zero savings, this is a signal to build your assets so your net worth will continue to grow. Put your money in savings and look at investment opportunities to grow your wealth.

No matter what stage you are in, regularly evaluating your net worth will give you an area of focus and provide an objective measurement of how you are progressing.

What Should Your Target Be?

Once you have calculated your net worth, your first thought will likely be… “So is that good or bad? How am I doing?”

The answer is…you are exactly where you are supposed to be. There is no “good” or “bad”. You might not be where you want to be with your net worth, but don’t beat yourself up over it. You’re just figuring this stuff out. Use it as fire under your feet to take action. You have arrived where you are today based on the knowledge and life experiences you’ve had to date. Now that you know what to do, you will be unstoppable!

It’s also important not to compare your beginning to someone else’s middle. If you look around and see others your age who have a much higher net worth than you, chances are they’ve probably been focused on this for a while. You will get there, but you have to start now.

How to Build Your Net Worth

The first step is to set your target. You can either look at the long-term view with how much money you need to retire in mind. Or you can look at your next milestone marker (ie. reach $1 or $100,000 net worth).

[bctt tweet=”You need three key ingredients to build your net worth: 1) time 2) regular contributions and 3) the power of compound interest.”]

Let’s say you invest $1000 today, and steadily add $100 each month. At the end of 20 years, you will have put in a total of $25,000. With an average 7% rate of return, you will have earned an additional $31,441 from the power of compound interest for a total investment value of $56,441. (Plug and play with your own numbers on NerdWallet’s Compound Interest Calculator.)

Compound interest will grow your money exponentially if you give it enough time to work. You need to start now, no matter where you are starting from, and automatically invest ideally 15% of your take-home (after tax) to build your net worth.

Net-Worth Building 101

What do do with your 15% net-worth building investment each month:

- If you have debt, put ALL this money (and more if you can) towards eliminating your debt as soon as humanly possible.

- If you have no debt, put your 10-15% towards building an Emergency Fund until you have a reserve of 6-month’s worth of living expenses.

- If you no debt and a 6-month Emergency Fund stored in a high-yield savings or money market account, you then direct that 10-15% towards an investment account, either a 401K, a Roth IRA, or an IRA, depending on your situation.

Do not wait until the market looks good to begin your investments. Start now. The timing will never be perfect, and even the best money managers can not accurately predict what will happen with markets. When you steadily invest a set amount every month into your investment accounts, you are employing a strategy called Dollar Cost Averaging, which means you will purchase more shares when prices are low and fewer shares when prices are high—a good strategy for long-term investments.

How will you know if you’re on track?

If your net worth is continually trending upwards, you are on the right track. There may be periods where market forces beyond your control will drive prices down and your net worth may stall or go down for a period. Do not panic. Leave your money where it is. Stay the course, and the market will rebound.

How to Monitor Your Net Worth

I use Personal Capital to track my Net Worth. This is a secure, online tool that provides a real-time, full-picture view of my financial situation. I link all of my financial accounts (checkings, savings, investment accounts, credit cards, loans, etc.) to Personal Capital and the software automatically gives me graphs and dashboards that show me my net worth, my portfolio allocation into my financial picture as a whole. There is a specific tab for monitoring Net Worth, and easy-to-understand graphs that help me visualize my progress.

I like that it has functionality that allows me to see my entire financial portfolio allocation and makes recommendations to consider for a more ideal allocation.

Now that you have some guidelines on how to measure your financial progress, it’s time to get started right now.

- Calculate your Net Worth as of today. This is your benchmark to measure future progress against.

- Set up your direct deposit or automatic transfers to your debt repayment, Emergency Fund or investment accounts. Put money in every month—no matter what.

- Complete your budget to give yourself a framework on how to save money

- Track your Net Worth at the end of month and hold yourself accountable and make sure you are trending up!