You may have heard of the term, but what exactly is dollar cost averaging? In the world of fancy investing lingo, I’ve found (to my pleasant surprise) that this complex sounding term actually explains a relatively simple concept.

Simply put, Dollar Cost Averaging is the systematic approach of investing a fixed amount of money, consistently, at regular intervals over a period of time. So if you have $10,000 to invest, a dollar cost averaging strategy might look like investing $1,000 each month over a 10-month period. With Dollar Cost Averaging, you stick with the steady investment intervals, regardless if the market is going up or down. This differs from Lump Sum Investing, in which you would invest all $10,000 at one time—ideally when stocks are priced low.

Why Would I Want to Use Dollar Cost Averaging?

Investing can feel scary. Dollar cost averaging gives us a way to manage risk. Here are five major benefits of a dollar cost averaging strategy:

- Avoid bad timing

Trying to time your entry/exit into markets can feel like gambling… because that’s what it often is. Even professionals who dedicate their careers to studying markets, misjudge markets when trying to time the market. - Ease your mind

The psychological and emotional stress of investing a large sum of money in a constantly moving market are real (see market timing above). Dollar cost averaging gives you a well-studied and savvy strategy to reduce the impact of market volatility on your investment. - Move confidently with an easy-to-follow structure

Dollar cost averaging is a strategy that helps you balance the lows and highs of the market. That ‘hot tip’ you read online is not a strategy—it is a best guess that may, or may not work. GameStop is the exception, not the rule. - Start compounding interest right away

If you are waiting to invest until you have a sizeable sum saved, your money is just sitting around, not doing anything for you. If you start today, with what you have, your money can start working right away, compounding dividends and growth immediately. - Realistic for everyone

You don’t need a statistics background, an advanced degree or a sophisticated and complex approach here. All you need is an investment fund and an automatic transfer set up on your account to get started. In fact, if you are investing in a 401K with every paycheck, you are already following a dollar cost averaging strategy!

It Can’t be That Simple, Can it?

When talking about the concept of dollar cost averaging, it’s all theoretical. So let’s take a look at the numbers to see it in action.

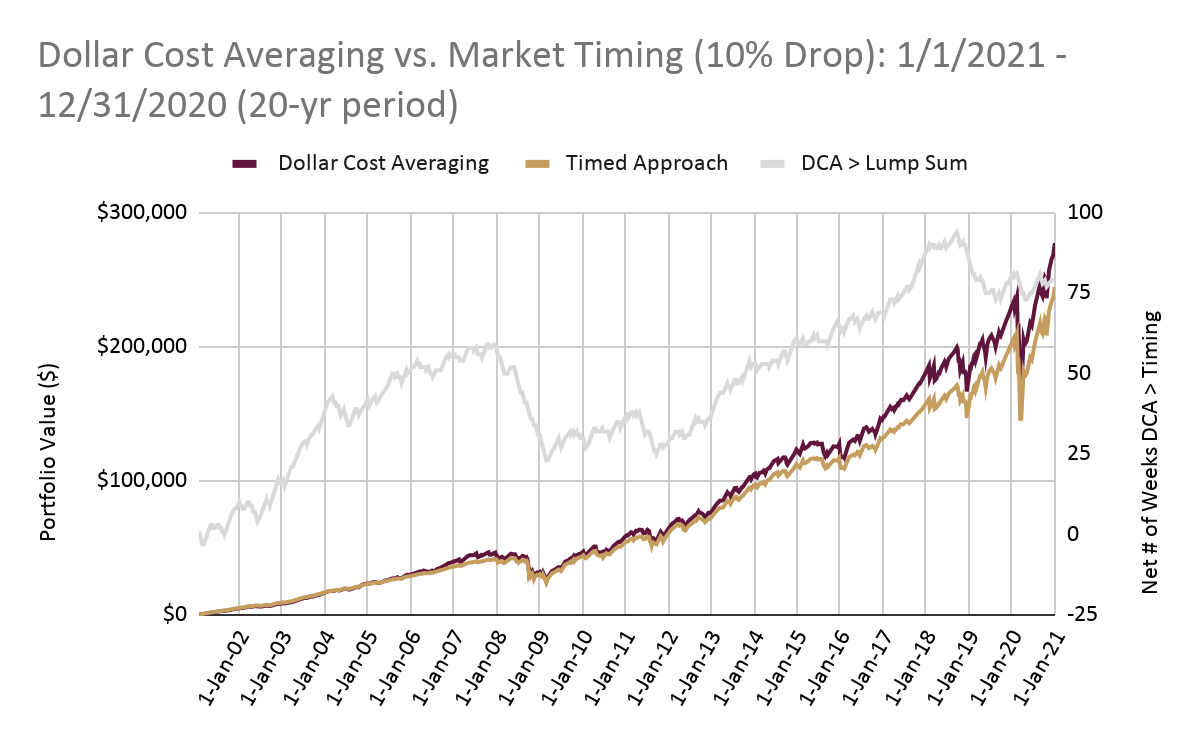

This example models portfolio performance looking at 20-year look back at S&P comparing a Dollar Cost Averaging strategy (maroon line) vs. Market Timing (gold line).

This graph is adapted from u/BestInterestDotBlog.

- Dollar Cost Averaging = $100/week invested into an S&P 500 index fund.

- Market Timing = $100 put into Savings Account and accumulated, and then invested once market dipped 10% from the previous high.

- DCA > Lump Sum = Net # of weeks DCA portfolio out-preformed Timed portfolio.

Over this period of time a Dollar Cost Averaging Strategy resulted in a portfolio value $19,391 (or 13.4%) higher than the timed market strategy, outperforming 561 weeks compared to the timed strategy that performed better 482 weeks… and unlike the Timed Market Strategy, Dollar Cost Averaging does not require you to constantly be monitoring the markets.

Are There Downsides to a Dollar Cost Averaging Strategy?

One argument against Dollar Cost Averaging is that while this approach helps reduce risk (by balancing the highs and lows of the market), that inherently means you are less likely to experience oversized returns.

When looking at major trends over long periods of time, a lump sum, or timed, approach historically has done better in bull markets, while dollar cost averaging tends to do better in bear markets…

…that said, it’s much easier to tell where these periods begin and end in hindsight.

Another point to keep in mind that the market tends to go up over time. If you are sitting on a lump sum of cash today, the faster you can get it into the market the faster it can start working for you.

On the other side of the coin, if you are starting from 0 today and looking ahead, your money will start working faster if you get it right to work with Dollar Cost Averaging, rather than waiting, for a potentially long time, for a significant market dip.

Finally in the cons list when it comes to dollar cost averaging, is potential for additional trading/transaction costs, depending on your selected investments, so look closely at your fund fees to ensure you are aware of all charges.

How to Pick the Right Strategy for You

If you are not interested in closely following markets and you want a solid strategy that can help protect you from large market swings, dollar cost averaging is a good approach for you.

If you already have a sum of money accumulated today that you are looking to invest, and if you are comfortable with a little more risk, you may want to consider investing a lump sum and then rebalancing your portfolio regularly. This will work best for you in a bull market..

If you’re unsure, find a good financial advisor who can work with you on your specific situation.

How to Get Started with Dollar Cost Averaging

If you know, for sure, you are ready to get started investing with a Dollar Cost Averaging strategy, a good place to start is your company 401(k) plan.

Related article: Should I Put Money in a 401(k) if There is No Company Match?

If you do not have a 401(k) available, you can open a brokerage account, and set up a recurring automatic monthly transfer into an index fund. Your regular contribution amount will stay the same, and the number of shares purchased will vary depending on the share price at the time of investment.

One very important caveat to remember… no strategy is a sure-win or a good substitute for picking a bad investment, so make sure you do your research to invest in something you understand and are comfortable with.

The great thing about the dollar cost averaging investment strategy is it’s available to everyone—right now. You don’t need to save up a large amount of money. You can start today with a steady contribution from every paycheck.